I. The End of ESG as Narrative. The Rise of Risk Architecture

By 2026, ESG has undergone a structural reclassification inside the enterprise.

It is no longer:

- a reporting function

- a sustainability initiative

- or a stakeholder communications exercise

It is now a core component of enterprise risk architecture.

The shift is not philosophical, it is operational.

Macroeconomic volatility, supply chain fragility, climate transition risk, and regulatory enforcement have converged to redefine ESG as pre-financial intelligence: a dataset that signals future balance sheet stress before it materializes.

In this context, ESG data that is incomplete, inconsistent, or unauditable is not neutral.

It is risk exposure.

II. ESG as a Financial-Risk Interface

At the center of this transformation lies the convergence of ESG with financial reporting frameworks.

The International Sustainability Standards Board (ISSB) has formalized ESG disclosures as financially material risk signals, requiring organizations to report how sustainability factors impact enterprise value.

Simultaneously, the Corporate Sustainability Reporting Directive (CSRD) extends this into double materiality, forcing organizations to measure both:

- Outside-in risk exposure (climate, regulation, supply chain disruption)

- Inside-out impact (emissions, labor practices, ecosystem effects)

This dual lens transforms ESG into a bidirectional risk model, where organizations must understand not only how risks affect them, but how their operations generate systemic risk.

III. ISO Standards as the Control Layer for ESG Risk

While ESG frameworks define disclosure requirements, ISO management systems provide the internal control environment required to generate reliable, audit-grade data.

This distinction is critical.

Without ISO-aligned processes, ESG reporting remains interpretive.

With them, it becomes verifiable.

Environmental Risk Controls

- ISO 14001

Establishes structured environmental risk identification, monitoring, and mitigation

- ISO 14064

Enables auditable carbon measurement across Scope 1, 2, and 3 emissions

- ISO 50001

Links energy performance to both emissions reduction and cost optimization

These standards transform environmental exposure into quantifiable operational variables.

Social and Governance Risk Controls

- ISO 45001

Converts workforce risk into measurable safety and incident metrics

- ISO 26000

Provides structure for human rights and stakeholder impact

- ISO 37001

Strengthens governance controls and corruption risk mitigation

Together, these frameworks create a system of internal ESG controls, analogous to financial internal controls under SOX.

IV. The Real Risk Surface: Supply Chains and Scope 3 Exposure

For most enterprises, ESG risk is not concentrated within their direct operations.

It resides in the value chain.

- Scope 3 emissions often represent 70–90% of total carbon footprint

- Human rights risks are embedded across multi-tier supplier networks

- Regulatory exposure increasingly extends beyond corporate boundaries

This makes supply chain transparency a critical risk management function, not a sustainability initiative.

Procurement as a Risk Control Function

ISO 20400 reframes procurement as a strategic ESG control mechanism.

It requires organizations to:

- integrate ESG criteria into supplier selection

- evaluate lifecycle impacts

- monitor supplier compliance and risk exposure

In this model, procurement becomes the execution layer of ESG risk governance.

V. The ESG Reality: Fragmentation, Backlash, and “Greenhushing”

Despite regulatory progress, ESG implementation remains uneven.

Regulatory Fragmentation

Organizations must navigate overlapping frameworks:

- ISSB (global baseline)

- CSRD / ESRS (EU)

- regional disclosure mandates (e.g., California climate laws)

This creates operational complexity and reporting duplication.

Political and Legal Pushback

In certain markets, ESG has become politically contested, particularly around:

- climate disclosures

- DEI metrics

- fiduciary duty interpretations

This has led to the rise of “greenhushing” — where companies continue ESG efforts internally but reduce public disclosure to avoid scrutiny.

The Assurance Gap

Most organizations are still operating at limited assurance levels, but the trajectory is clear:

- movement toward reasonable assurance

- increased third-party verification

- tighter regulatory enforcement

This will require ESG data systems to meet audit-grade standards equivalent to financial reporting.

VI. The Technology Inflection Point: From Reporting to Intelligence

The complexity of ESG data has outgrown manual systems.

Spreadsheets cannot handle:

- multi-tier supplier data

- real-time emissions tracking

- regulatory alignment across jurisdictions

This has triggered a shift toward digital ESG infrastructure.

AI-Driven ESG Systems

Advanced systems now enable:

- automated data ingestion across suppliers

- anomaly detection in ESG metrics

- predictive risk modeling

This transforms ESG from retrospective reporting into forward-looking risk intelligence.

Integrated Reporting Architecture

The future state is clear:

- ESG data integrated into ERP systems

- real-time dashboards for risk monitoring

- machine-readable disclosures (XBRL)

In this model, ESG becomes a continuous data stream, not an annual report.

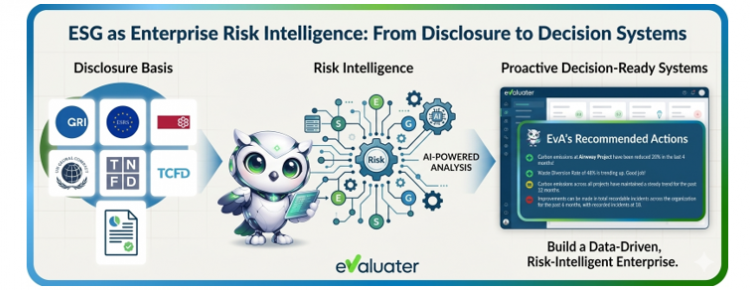

VII. Strategic Enablement: How eValuater Supports ESG Reporting at Scale

For sustainability and risk leaders, the core challenge is no longer understanding ESG.

It is operationalizing it across complex organizations and supply chains.

This is where eValuater plays a critical role.

From Fragmented Data to Decision Intelligence

eValuater acts as an ESG intelligence layer, consolidating data across internal systems and supplier networks.

It enables organizations to:

- identify ESG risk concentrations

- map supply chain vulnerabilities

- prioritize mitigation strategies

Automated, Audit-Ready Data Collection

The platform replaces manual ESG data processes with:

- standardized supplier assessments

- automated data validation

- continuous monitoring

This significantly improves data accuracy, consistency, and audit readiness.

ISO-Aligned ESG Governance

eValuater integrates ESG evaluation with ISO frameworks, allowing organizations to align reporting with:

- environmental management systems

- procurement standards

- governance controls

This ensures ESG data is not only collected, but structured according to globally recognized management systems.

Scope 3 and Supply Chain Visibility

One of the most critical capabilities is deep supply chain intelligence.

eValuater enables organizations to:

- assess ESG performance beyond Tier-1 suppliers

- estimate and track Scope 3 emissions

- detect high-risk suppliers early

This transforms supply chain ESG from a blind spot into a manageable risk domain.

From Reporting to Action

Most importantly, eValuater bridges the gap between:

- ESG reporting

- and operational decision-making

It allows organizations to integrate ESG insights into:

- procurement strategies

- risk management frameworks

- investment decisions

VIII. Conclusion: ESG as the New Risk Operating System

The evolution of ESG is no longer about sustainability positioning.

It is about enterprise survival in a risk-saturated environment.

Organizations that succeed will not be those with the best narratives.

They will be those with:

- the most reliable data

- the strongest internal controls

- the deepest supply chain visibility

- and the ability to translate ESG signals into strategic decisions

ISO standards provide the control framework.

Regulations provide the disclosure requirements.

Platforms like eValuater provide the intelligence layer.

Together, they form the foundation of a new reality:

ESG is no longer a report.

It is the operating system of resilient enterprises.